It started with a family dinner argument.

One side of the table: “FD is safe. Always has been.”

Other side: “SIP is the only way to actually build wealth.”

Sound familiar?

This debate plays out in millions of Indian households every year. And honestly, both sides have a point — depending on what you’re trying to achieve.

So instead of opinions, let’s look at what history actually shows us.

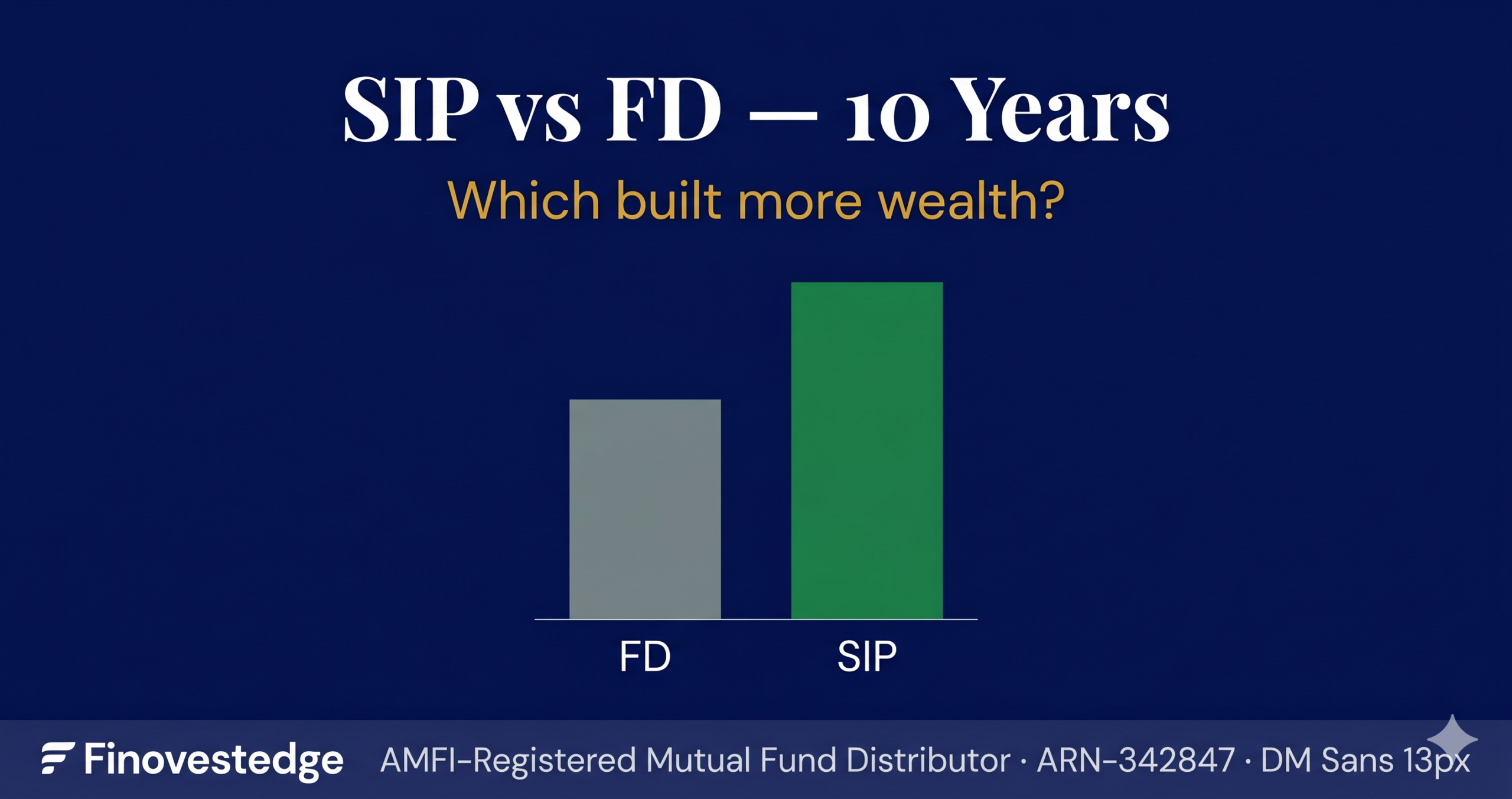

The Comparison: Same Money, Two Paths

Let’s take a simple, real-world scenario:

A salaried professional in their early 30s. ₹10,000 to invest every month. A 10-year horizon — roughly what it takes to hit real

goal-based investing milestones like a child’s education, a home down payment, or a strong retirement head start.

Two choices:

→ Put ₹10,000/month into a bank Fixed Deposit (FD)

→ Put ₹10,000/month into a diversified equity mutual fund via SIP

Total invested in both cases: ₹12,00,000 (₹12 lakhs) over 10 years.

What happened next is where the stories diverge.

What the Numbers Have Historically Shown

Based on historical broad market data and commonly available FD rates over the past decade, here is how the two approaches have typically compared:

Note: These are illustrative figures only, based on historical averages of broad market benchmarks and typical bank FD rates. Actual returns will vary. Mutual fund returns are not guaranteed. FD rates are subject to change. This comparison does not recommend any specific scheme or product. For your own projections, use AMFI’s SIP calculator — it uses actual fund data and is free to access.

Why Does This Difference Happen?

Three forces create this gap over time. Understanding them is more valuable than any single number.

1. The Power of Compounding — But Differently

Both FD and SIP benefit from compounding. But they compound differently.

An FD compounds at a fixed rate on a fixed sum — predictable, steady, capped.

An equity fund compounds on a growing base, where the underlying businesses you’re invested in also grow their earnings over time. When markets perform well over long periods, this creates a snowball effect that a fixed rate simply cannot match.

The longer the horizon, the wider this gap historically becomes.

2. Inflation: The Silent Thief

India’s average consumer inflation over the past decade has hovered between 5–6% per year.

A 7% FD return, after tax (FD interest is fully taxable as per your income slab), can leave you with a real return of just 1–2%. In other words, your money grows — but barely faster than prices rise.

Equity mutual funds, over long horizons, have historically had a better chance of generating returns that stay meaningfully ahead of inflation.

This doesn’t make FDs bad. It makes them suitable for specific purposes — which we’ll come to.

3. Rupee-Cost Averaging: SIP's Hidden Advantage

When markets fall, your ₹10,000 SIP buys more units. When markets rise, those extra units increase in value.

This is rupee-cost averaging — and it’s one of SIP’s most powerful structural advantages over a lump sum or an FD.

You don’t need to time the market. You don’t need to predict corrections. The mechanism works quietly, month after month, in your favour.

The Real Risk Nobody Talks About

Here’s something data doesn’t capture easily: investor behaviour.

The biggest risk in equity investing isn’t a market crash. It’s what you do during a market crash.

Historically, investors who stopped their SIPs during downturns (2008, 2020, early 2022) locked in their losses and missed the recovery. Investors who stayed the course — who treated a falling market as a discount sale — came out significantly ahead.

This is why at Finovestedge, we say: behaviour is the real edge.

An FD removes this variable entirely — your returns don’t depend on your emotions. That’s not a weakness. For money you genuinely cannot afford to see fluctuate, an FD’s predictability is a feature, not a bug.

The question is: which money is which?

When FD Is Actually the Right Answer

We want to be clear: this is not an article telling you FDs are bad.

FDs are the right tool for:

→ Emergency fund (3–6 months of expenses) — you need certainty here

→ Short-term goals (under 3 years) — equity markets can be volatile over short periods

→ Capital you absolutely cannot risk — elderly parents’ savings, medical funds

→ Investors who cannot emotionally handle NAV fluctuations

The goal is not to pick a “winner.” The goal is to match the right instrument to the right purpose.

The Honest Answer to the Question

If your goal is 10 years away or longer — a child’s higher education, retirement, financial independence — historical data consistently shows that staying invested in diversified equity via SIP has built meaningfully more wealth than FDs over comparable periods.

If your goal is 1–3 years away, or the money is your safety net — an FD or a short-term debt fund is more appropriate.

Most families need both. The trick is knowing which money goes where — and staying consistent with the long-term portion even when markets test your nerves.

That, ultimately, is the edge.

Want to see the numbers for your own monthly amount?

Use our SIP calculator to model your own scenario.

Not sure where to start?

If you’re unsure whether your current mix of FDs and SIPs is aligned with your actual goals — we can help you think it through. No jargon, no pressure.

Disclaimer: This article is for educational and informational purposes only. All return figures mentioned are illustrative estimates based on historical broad market data and are not indicative of future returns. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Fixed deposit rates are indicative and subject to change by individual banks. This article does not constitute investment advice and does not recommend any specific mutual fund scheme, fund house, or financial product. Finovestedge Distribution Private Limited (ARN-342847) is an AMFI-registered Mutual Fund Distributor — not a SEBI-registered Investment Adviser (RIA). For personalised guidance, please consult a qualified financial professional.

AMFI Helpline: 1800-22-6868 | SEBI SCORES: scores.sebi.gov.in

Finovestedge Distribution Private Limited | ARN-342847 | finovestedge.com